What is Marginal Cost in Economics?

Here we understand the meaning and concept of Marginal Cost in detailed with example.

Do you have similar website/ Product?

Show in this page just for only

$2 (for a month)

0/60

0/180

What is Marginal Cost in Economics?

Meaning of Marginal Cost:

Marginal Cost is addition to the total cost caused by producing one more unit output. In other words, it means that marginal cost is the addition to the total cost of producing 'n' units instead of n - 1 units, where n is any given number. Thus,

MC = TCn - (TCn-1)

It clearly indicates that the marginal cost is independent of the amount of fixed cost. Since fixed costs do not change with output, there are no marginal fixed costs when output is increased in the short run period time. It is the variable cost that varies with the output in the short period. Changes occurs in marginal cost are therefore, due to change in variable cost. Marginal cost is not affected by the amount of fixed cost.

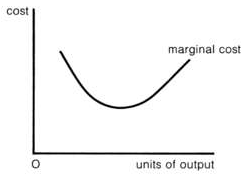

Figure -

Like the average cost, the marginal cost also falls in the beginning, reaches its minimum and then starts rising as shown in above figure.

The fall in the marginal cost in the beginning is because of the operation of the law of increasing returns.

Same way, the rise in marginal cost after a point is because of the operation of the law of diminishing returns.

Now, we understand this concept more clearly with the help of example-

Suppose the total cost (TC) of manufacturing 100 units of output is Rs. 100/-. Now if the total cost increases from Rs. 100/- to Rs 111/- by producing 101, i.e. one more unit, the Marginal cost (MC) is Rs. 11/.

Marginal cost can be worked out using the following equation as follows-

MC = TCn - TCn-1

Where,

MC = Marginal cost

TCn = Total cost of 'n' number of units of output.

TCn-1 = Total cost of 'n-1' units of output.

If TCn = Rs. 111, TCn-1 = Rs. 100

MC = Rs. 11.

CONTINUE READING

Marginal Cost

Kinnari

Tech writer at NewsandStory